|

The rapidly evolving and digitisation of the African economy isn’t completely aligned to the sheer volume of the population who remain unbanked and continue to lack access to basic financial services. Having experienced these challenges herself, Elorm Axolu, founder of Xpendly, decided to do something about it. In today’s Afritech XYZ conversation, Bayo Adelaja finds out how Xpendly came to be.

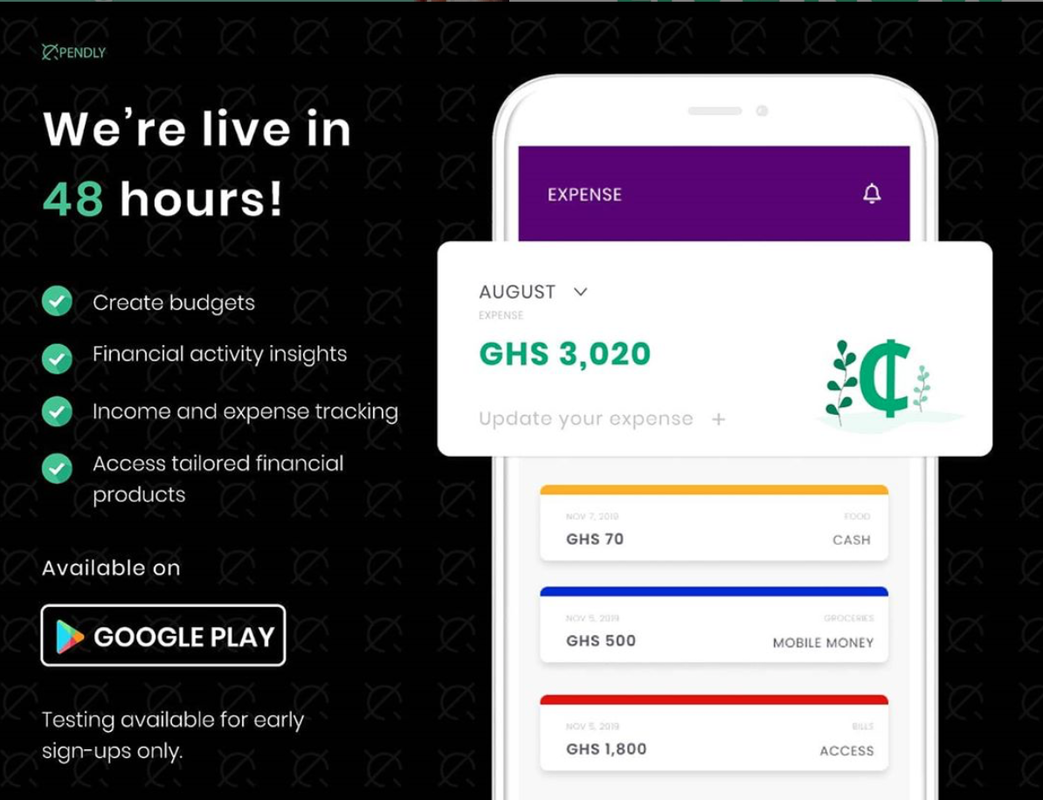

Xpendly helps users organise their money by helping them create customised budgets, enabling them to track income and expenses and delivering insights on their overall financial activities. The data it collects is used to sketch out a profile of users’ credit rating, rather than using traditional sources of data such as historical credit purchases, which its users typically don’t have. With most users lacking formal financial records, social media and employment information is used as a means of credit assessment and assessing ratings. The app also pulls data from the user’s transaction history, including data from cash inflow, expenses, and other user behaviour to update credit ratings. The app further integrates users’ bank cards and accounts, if available, which feeds the app’s capacity to track and analyse user activity.  Xpendly won the Ghana Tech Lab competition and decided to target its solution at consumers, having had first-hand experience of what it’s like to try and prove credit-worthiness themselves. The app has elements that are free, with its revenue coming from premium add-ons, commissions and in-app advertising. Its aim is to grow the business into a credible financial data company, therefore continually collecting quality data is a core driver of their business activity. Elorm tells us that being part of supportive tech hubs such as the Ghana Tech Lab and Afritech XYZ is essential for the support and mentorship they receive during their founder journey. Building up a database of a wide range of customer profiles, accurately based on user behaviour, should lead to lower fees and a fairer system of credit rating. The cycle of poverty that can exist due to consumers’ inability to borrow money when they need it and financial institutions being unable to lend money due to lack of financial data should eventually also diminish. Comments are closed.

|

Archives

September 2023

|

RSS Feed

RSS Feed